Equity Analysis: Consensus Mining & Seigniorage Corporation (CMSG)

A digital asset compounding machine targeting a 36x from $25/share to $900/share by 2036.

May 2, 2026

What it does: CMSG is a cryptocurrency mining company that aims to increase its bitcoin per share, with no debt, and no dilution.

About the Company

I’m going to refrain from explaining why Bitcoin is a good long-term asset, as that is a different topic, and one that I do think everyone needs to explore. CMSG is unique as it owns machines that mine cryptocurrency at a cheaper cost than it would be to purchase on the open market. They pay hosting and electricity fees, and minimal SG&A. This creates a long-term ‘seignorage’ profit of a scarce asset, that accrues and grows on the balance sheet forever. Essentially, you are taking depreciable equipment to create an infinite, appreciating asset. They are different than other cryptocurrency miners because they don’t dilute or use leverage to chase the cycle and have a conservative capital structure that aims to optimize their ROIC over time. This model is unique in that we see scarcity layered on scarcity like this, where Bitcoin has a fixed issuance, while the number of shares in CMSG is also a fixed amount.

Right now, it is laughably cheap as it trades on OTCQX, people don’t truly understand the model, and it is pretty illiquid with only a few hundred shares trading each day (last week there was a day where I was the only liquidity with 2 shares purchased). There is no coverage, and I think over the next 10 years, this could be one of the most compelling investments you can hold.

What It Owns

First, let’s start with the balance sheet just to explain a few things. This is always where I start when underwriting a business.

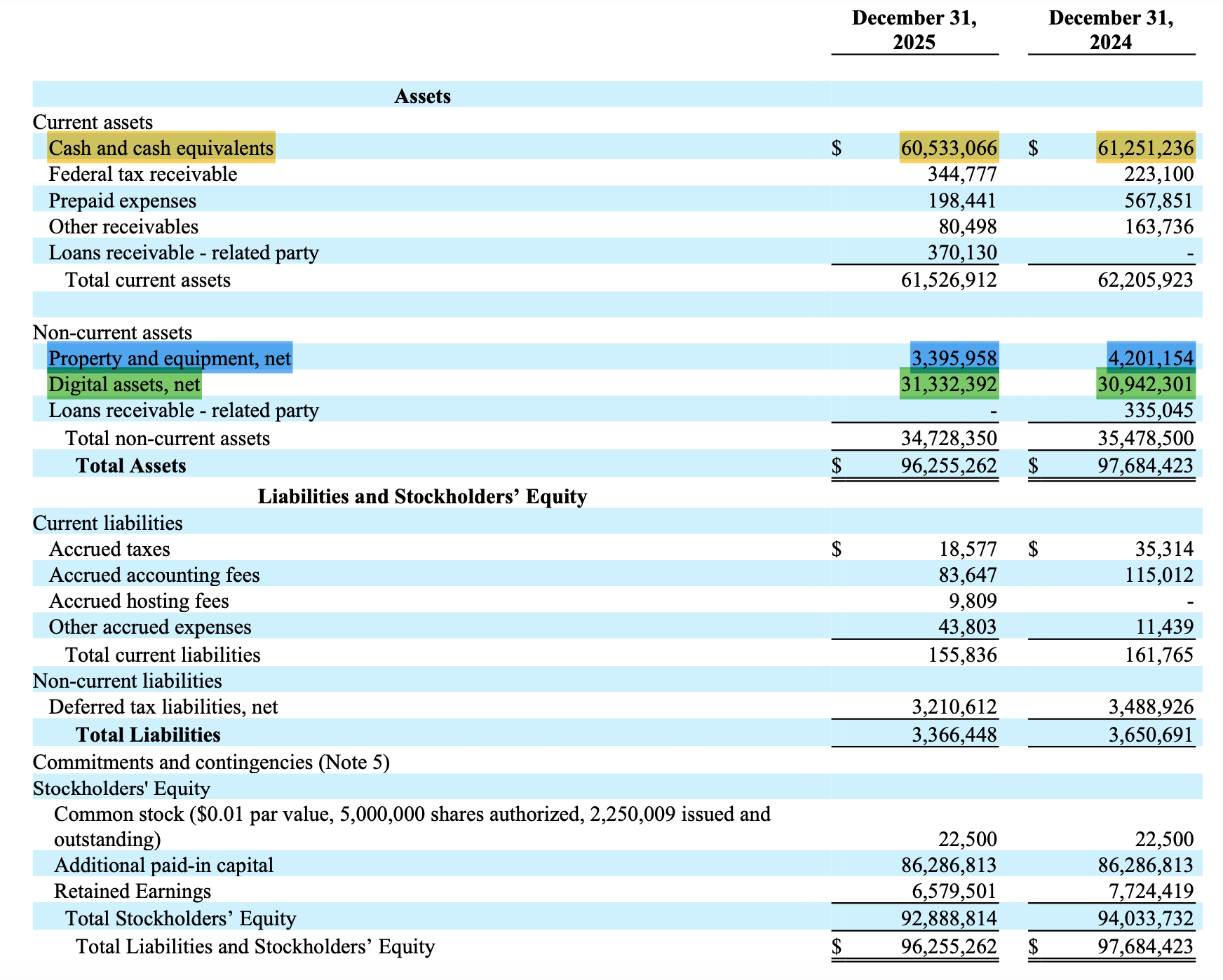

Cash: CMSG has $60m of cash on its balance sheet. The entire market cap of the company as of writing is $56m. Trading below the cash portion of its balance sheet. It uses this cash to add to its equipment over time and keep a reserve to maintain liquidity and zero debt. This alone is great, especially to ride out the volatility of the cryptocurrency ecosystem.

PP&E: It has around $3.4m worth of cryptocurrency mining devices that help to mine new coins every minute of every day. Depending on depreciation and based on equipment cycles, this will increase and decrease, but equipment is slowly purchased every quarter.

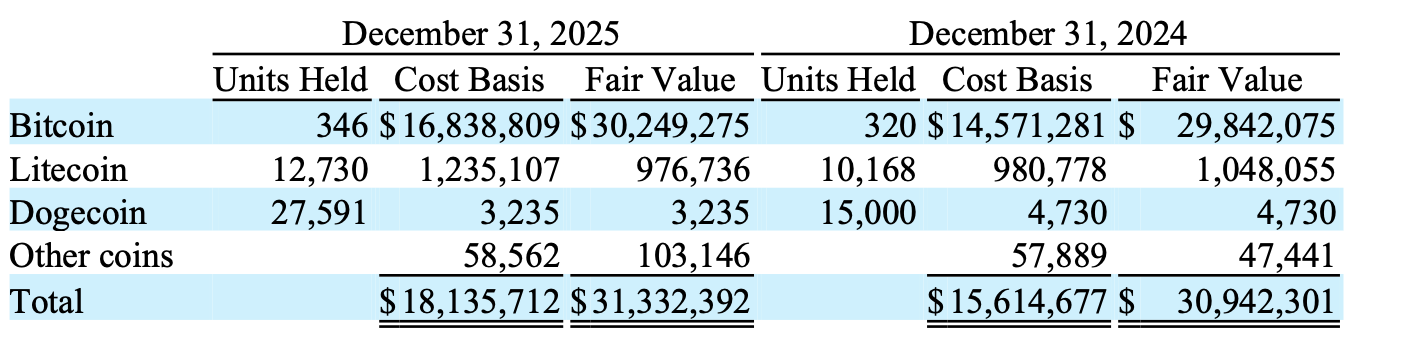

Assets: It has around $31.3m of digital assets. From 2024- 2025, the dollar value of the digital assets has remained the same, but over that time, they have increased the number of coins they hold, as the price of bitcoin itself has decreased. (Added 26 bitcoin to their balance sheet from 2024-2025 , or from 320 to 346 bitcoin).

Debt: Effectively no debt. All of their liabilities are deferred tax liabilities (essentially capital gains on their appreciated Bitcoin).

The Business

The big idea here is that from when the company started in 2021, it started with around 115 Bitcoin. By the end of 2025, they held 346 Bitcoin and 12,730 Litecoin. This was done organically through mining, with no debt, and no dilution of shares. This is what you need to know.

In 2024, they held 320 bitcoin and 10,168 litecoin. Growing their stack 8.1% and 25.1% of Bitcoin and Litecoin, respectively over the course of the year. All while maintaining $60m of cash, no debt, and no dilution. When cryptocurrency prices are depressed, the difficulty of the Bitcoin network decreases, and they mine more coins, providing a hedge to the equity holder as those coins appreciate as the market reverses. Over time, this is a digital asset treasury that grows through mining, while maintaining a conservative capital structure. How would one value that business that is growing its underlying asset base at 8% annually while the asset itself is appreciating at 25-30% CAGR? More on valuation below. Other digital asset treasuries use some combination of debt or dilution and won’t be sustainable in the long run.

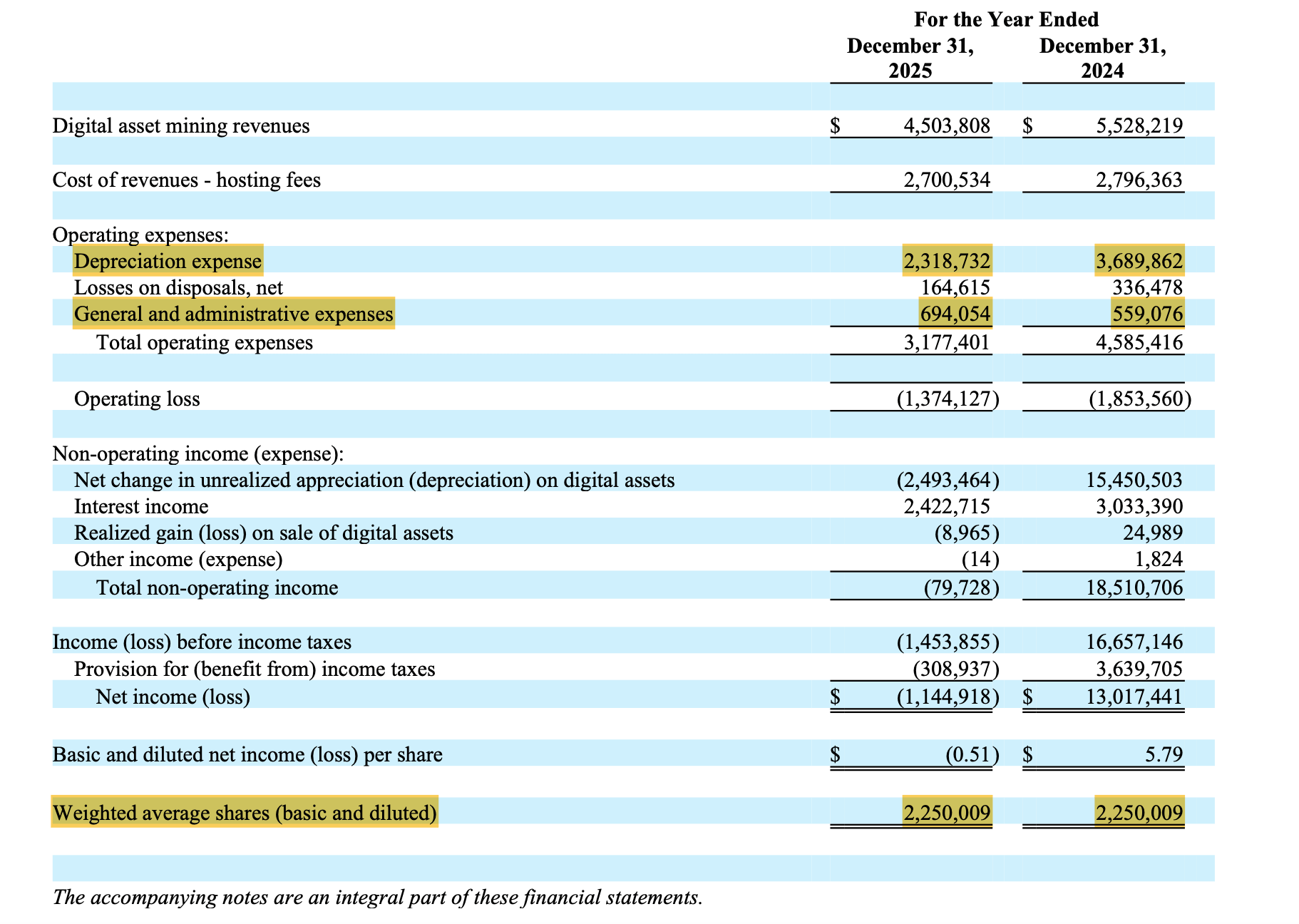

CMSG also has low administrative costs as the team at Horizon Kinetics run this company, and there is a minimal SG&A charge, so all the assets mined are effectively going to the bottom line.

The operating loss in this company is not relevant, as the assets they mine sit on the balance sheet and grow. Depreciation expense is also a part of the cryptocurrency mining business, as machines must be replaced, but again, you are using a depreciable asset to create a scarce, infinite-duration asset. Well worth it in my opinion.

You don’t need to believe that they will grow their business into new markets, get new customers, or what have you. This is business governed by the Bitcoin protocol, and they have great hosting and equipment relationships, having been in the industry for over a decade. This is a long-term compounder with high insider ownership and no dilution. It is a better way to own Bitcoin, as the mining provides a hedge to the downside, as you can acquire more coins over time, over a fixed share count.

Scrypt Mining

The company has been acquiring machines the past several quarters that run the Scrypt mining algorithm. These devices mine both Dogecoin and Litecoin with the same electric current, and because there is no halving with Dogecoin, the theory is that these devices will last longer and provide steady income to cover hosting expenses, and purchase Bitcoin at a lower price than on the open market. It also mines Litecoin effectively for free as a function of selling the Doge. This is the hidden call option as there is a ton of volume across the Litecoin network compared to Bitcoin, and in a world of instant settlement, Litecoin’s blocks settle every 2.5 minutes instead of every 10 minutes like Bitcoin’s. With a larger supply cap than Bitcoin, it effectively has the same monetary protocol, and if it ever finds a use case, the upside here could be startling. My analysis here assumes this doesn’t happen as the economics are already compelling. Add modest or significant price appreciation to Litecoin over the next decade, and things get very interesting.

Valuation

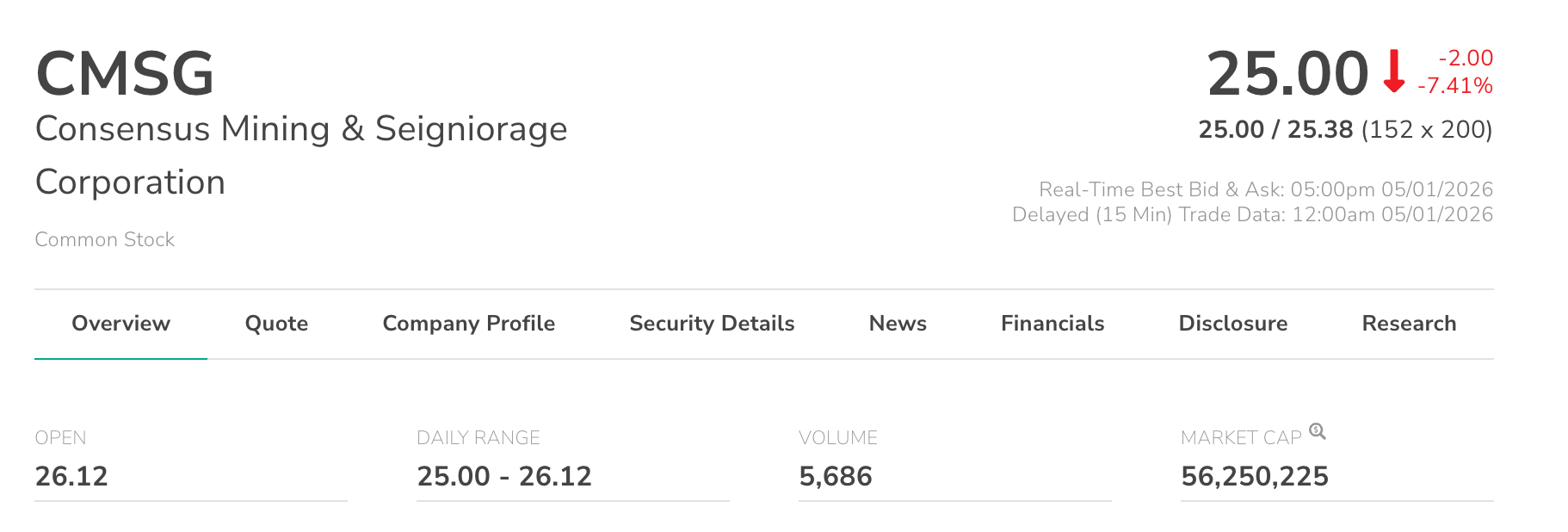

Right now, the company is valued at $25/ share or $56.25m market cap.

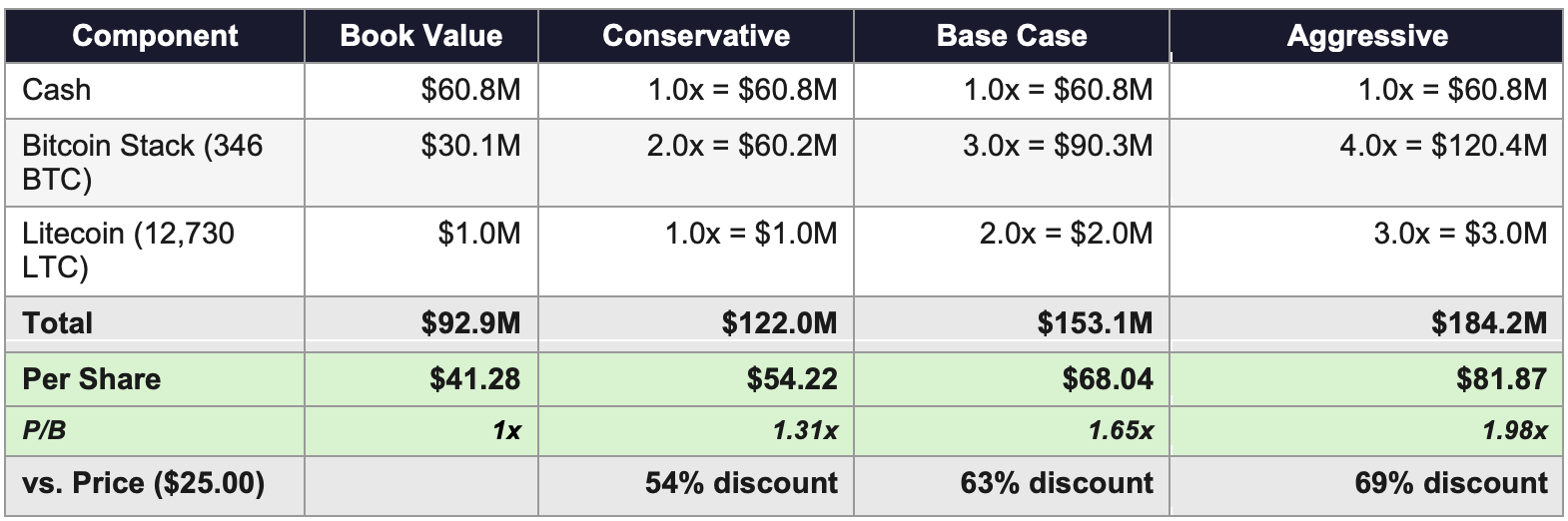

The company provides a book value figure, and over time, it is clear that with a company growing its assets at this pace, it should trade at a premium to book value. At the end of 2025, the book value per share was $41.28. And trading at $25, at a 40% discount to its book value. For a company that is growing its Bitcoin stack organically, this deserves a premium.

Next, let’s take a look at how things should trade in a rational environment:

What Is Each Asset Actually Worth?

Traditional P/B analysis applies a single multiple to the entire book value. This is misleading when 65% of the balance sheet is cash (which deserves 1.0x) and 32% is Bitcoin (which deserves a premium for structural reasons unique to this vehicle). The correct approach values each component separately.

Why the Bitcoin Stack Deserves a Premium to Spot Price:

The multiple on the Bitcoin & Litecoin stack reflects four structural advantages that do not exist in an ETF or direct custody:

Self-growing treasury. The mining operation adds approximately 26 BTC and 2,600 LTC per year to the balance sheet. Electricity is funded entirely by Dogecoin sales. Dogecoin has no halving, so the funding mechanism runs indefinitely. The Bitcoin count grows roughly 8% annually at zero cost to shareholders.

Zero debt. No forced liquidation during drawdowns. No margin calls. No covenant violations. When Bitcoin dropped 75% in 2022, leveraged holders were wiped out. CMSG held through with zero solvency risk.

Zero dilution. 2,250,009 shares outstanding. Fixed. Every bitcoin mined accrues entirely to existing shareholders. No dilution, no debt. No stock-based compensation dilution.

Anti-fragile accumulation. When Bitcoin crashes, marginal miners exit the network, difficulty adjusts downward, and CMSG mines more Bitcoin per day because it represents a larger share of the total network hashrate. The treasury grows faster during bear markets. Book value after recovery exceeds pre-crash levels. Unfortunately, in Bitcoin bear markets, book value compresses as the market is unsure about the future price of the underlying Bitcoin (hence why it is trading at a massive discount to book value currently). This is pretty standard across other miners and treasury companies as well.

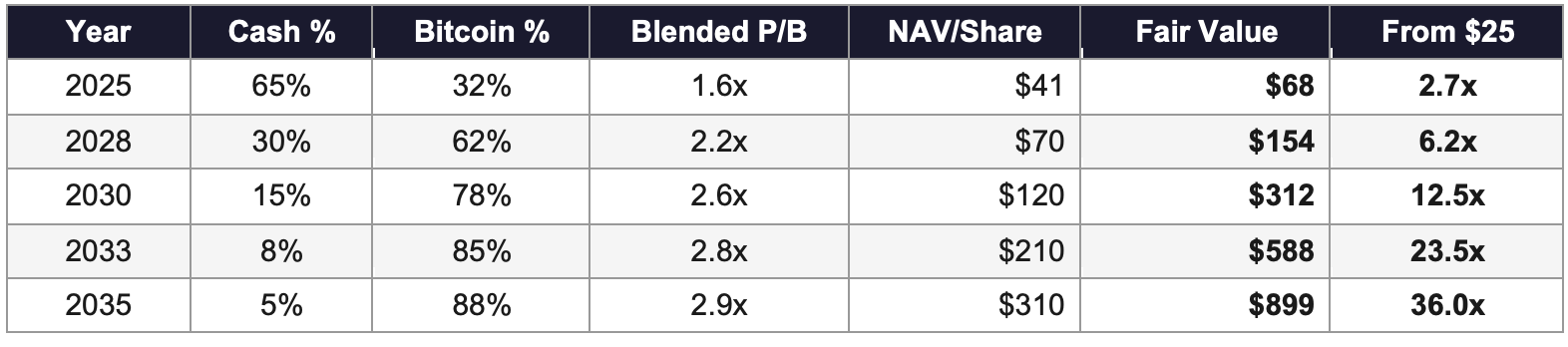

The Compounding Multiple

As cash converts to Bitcoin through mining and open market purchases with Scrypt mining profits, the balance sheet composition shifts. Since the Bitcoin on the balance sheet deserves a higher multiple than cash, the blended fair P/B on total NAV rises automatically over time. The multiple compounds.

Three Simultaneous Compounding Engines:

Engine 1: Bitcoin price appreciation (~25% CAGR conservatively). Supported by halving schedule, thermodynamic limits on mining efficiency as chip efficiency is plateauing, and institutional adoption.

Engine 2: Mining adds Bitcoin to the treasury (~8% annual quantity growth). 26 BTC per year accumulated at zero cost to shareholders. Over 10 years, the BTC count roughly doubles from mining alone.

Engine 3: Balance sheet composition shift (~3-5% annual multiple expansion). As cash converts to Bitcoin, the justified P/B rises automatically without any management decision.

Combined effective return: ~35% CAGR on the bitcoin stack. Over the next decade, at a P/B ratio of ~3, this represents a 36x return from today’s $25 share price, with these assumptions. This is very conservative if you assume the company doesn’t acquire another business, Litecoin doesn’t appreciate materially, or they don’t realize other efficiencies that improve their accumulation rate. Each one of these vectors could enhance the return profile. It should also be noted that presently, the market is penalizing the company for the excess cash on balance sheet (this is a plus in my opinion) and trading OTC. Both resolve over time.

Key Assumptions

Bitcoin Price CAGR: 25% (conservative end of historical range)

Mining rate: 26 BTC per year (current pace, may increase with increased efficiency and/or scale)

Share count: 2,250,009 (fixed, never diluted)

This assumes Bitcoin is $700,000 by 2036 (modest in my opinion).

Assumes that Litecoin does not find a use case. Litecoin is the free call option as they acquire at zero cost via Scrypt mining. If Litecoin price increases materially, then CMSG compounds further then our outline above.

Debt: $0 (no leverage, no margin calls, no forced liquidation)

Operating costs: Covered by Dogecoin sales (no halving on DOGE = perpetual funding)

Finally, if one were to buy $10,000 of Bitcoin today, they would own .12769 BTC at a price of $78,311 as of May 2. They would also own .12769 BTC in 2036. Granted it would be worth more in USD, but same amount of BTC.

Now consider a $10,000 of investment in CMSG today. That purchase is 400 shares at $25/share. Each share today has a claim to 0.00015377716 BTC. At 400 shares, that’s 0.061510864 BTC. About half of what you would get at just buying BTC in the open market (since most of balance sheet is cash today).

Now consider the year 2036, with those same 400 shares of CMSG. Mining more Bitcoin has been taking place, accumulating 8% more BTC annually resulting in a total stack of 747 BTC. Those 400 shares now have a claim of 0.1327994688 BTC. Litecoin per share is added as well, which we haven’t calculated, and a clear share premium to those underlying assets, compounding the investment. Another 10 years and the BTC/share increases further.

The big idea is you end up with more Bitcoin and an operating business by buying CMSG than you would than by buying Bitcoin directly.

Time Required

This is a very illiquid stock trades on OTCQX. The price could stay here for years and then gap up upon the above analysis. I have no prediction on when this will be, nor do I care. Quite frankly, I like that it is thinly traded, as I can acquire a few shares every day. This is a business I can understand, as I own some machines and mine myself, and understand the edge that this team has. An uplisting, acquisition, or some other catalyst will help price meet value. You don’t have to believe a lot to understand that value will eventually be recognized here. As you know, I’ll wait forever as I’m in no rush. Nothing to rush to.

Disclaimer: I am not a financial advisor, broker, or licensed investment professional. Nothing in this article constitutes investment advice, a recommendation to buy or sell any security, or an offer to transact. This is independent research reflecting my personal analysis and opinions. I hold a long position in CMSG. My views are inherently biased by my ownership. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. The valuations and projections presented are based on assumptions that may prove incorrect. CMSG is a micro-cap, OTC-traded security with extremely limited liquidity — shares may be difficult to buy or sell at desired prices. Do your own research and consult a qualified financial advisor before making any investment decisions.

Life & Capital — lifeandcapital.substack.com

Great insight man, actually interesting

Subscribed, would love to have you along too 🙂🙌